Markets in Hong Kong and mainland China rise on stronger industrial profit signals and renewed technology momentum, while positioning around CATL shifts sharply after heavy share sales.

SYSTEM-DRIVEN dynamics in China’s equity market—shaped by industrial profit trends, liquidity flows, and technology sector sentiment—drove a broad but uneven advance in Hong Kong and mainland Chinese shares, as investors reassessed growth expectations and risk positioning across heavyweight stocks.

What is confirmed is that Chinese and Hong Kong equities edged higher in recent trading sessions, supported by improving industrial profit data and a renewed appetite for technology-linked assets.

The benchmark Hong Kong indices gained modestly, with tech-heavy segments outperforming broader benchmarks at various points, reflecting a shift back toward growth-oriented stocks after periods of profit-taking and volatility.

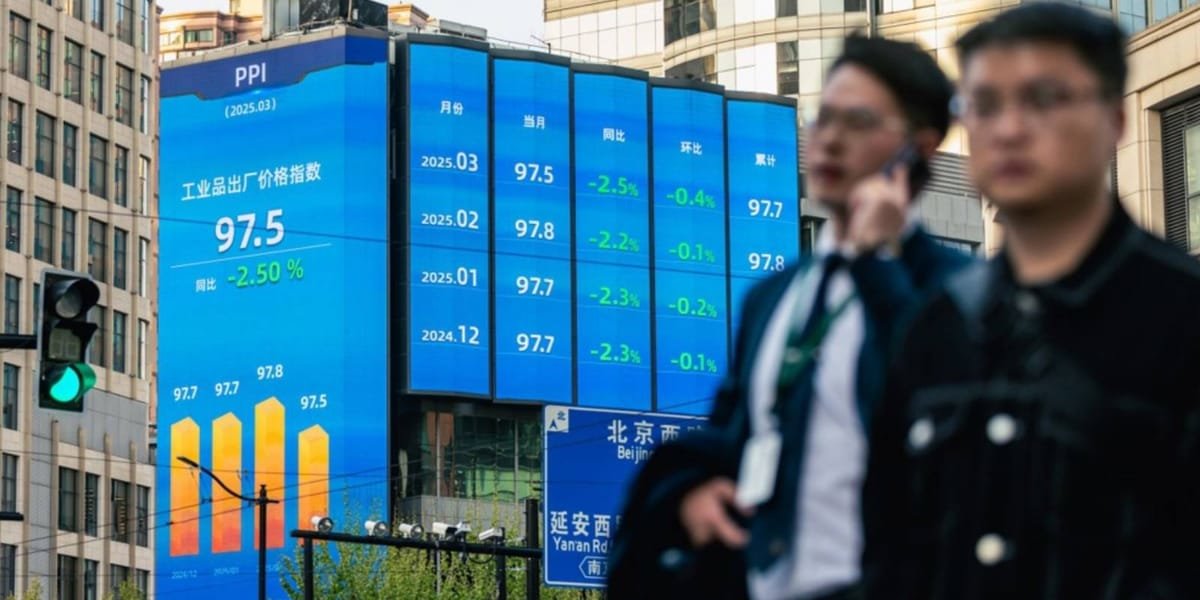

The immediate macro driver was fresh industrial profit data from China, which signaled stabilisation in corporate earnings after a prolonged period of uneven recovery.

While not a uniform rebound across sectors, the data was strong enough to reinforce expectations that China’s manufacturing base may be regaining momentum, particularly in export-linked and high-end industrial segments.

This provided a supportive backdrop for equity markets that have been sensitive to growth uncertainty and policy direction.

Technology stocks played a central role in the upward drift.

Investors rotated back into large-cap tech names listed in Hong Kong after recent pullbacks, encouraged by improving sentiment around artificial intelligence, electric vehicles, and semiconductor supply chains.

The Hang Seng Tech index, which has been volatile throughout the year, showed relative strength compared with the broader market, indicating that risk appetite remains concentrated in innovation-linked equities rather than cyclical consumption sectors.

A key parallel development was the sharp shift in positioning around Contemporary Amperex Technology Co., the world’s largest electric vehicle battery producer, which is dual-listed in Shenzhen and Hong Kong.

Following a large-scale share sale that expanded available float, bearish positioning against the Hong Kong-listed shares fell significantly.

Market data showed short interest dropping to its lowest level in months, as traders unwound positions that had previously profited from valuation gaps between Hong Kong and mainland listings.

The share sale itself acted as a liquidity reset.

By increasing the supply of borrowable shares, it reduced the cost of shorting and enabled hedge funds and macro traders to exit crowded bearish trades.

At the same time, it signaled continued corporate confidence in funding expansion and international growth, particularly in battery manufacturing capacity and next-generation energy storage technologies.

Importantly, the reduction in bearish bets does not imply a uniform bullish consensus.

Instead, it reflects a repositioning after a period of extreme concentration in short trades tied to valuation spreads between dual-listed Chinese equities.

With that arbitrage pressure easing, CATL’s Hong Kong shares have stabilised near elevated levels, supported by continued investor focus on electric vehicle demand, energy transition policies, and global supply chain expansion.

Across the broader market, the interaction between macro data and stock-specific flows remains decisive.

Industrial profit improvements provide a baseline signal of stabilisation, but equity performance is still heavily influenced by liquidity conditions, regulatory expectations, and global risk sentiment toward Chinese assets.

The combined effect of stronger industrial earnings signals and easing bearish pressure in key growth stocks has therefore produced a cautious but visible uplift in Hong Kong and mainland equities, with technology and advanced manufacturing sectors leading relative performance.

Market participants are now positioning around whether this phase represents a durable earnings recovery or a temporary repricing driven by liquidity shifts and short-covering activity in high-profile growth stocks.

What is confirmed is that Chinese and Hong Kong equities edged higher in recent trading sessions, supported by improving industrial profit data and a renewed appetite for technology-linked assets.

The benchmark Hong Kong indices gained modestly, with tech-heavy segments outperforming broader benchmarks at various points, reflecting a shift back toward growth-oriented stocks after periods of profit-taking and volatility.

The immediate macro driver was fresh industrial profit data from China, which signaled stabilisation in corporate earnings after a prolonged period of uneven recovery.

While not a uniform rebound across sectors, the data was strong enough to reinforce expectations that China’s manufacturing base may be regaining momentum, particularly in export-linked and high-end industrial segments.

This provided a supportive backdrop for equity markets that have been sensitive to growth uncertainty and policy direction.

Technology stocks played a central role in the upward drift.

Investors rotated back into large-cap tech names listed in Hong Kong after recent pullbacks, encouraged by improving sentiment around artificial intelligence, electric vehicles, and semiconductor supply chains.

The Hang Seng Tech index, which has been volatile throughout the year, showed relative strength compared with the broader market, indicating that risk appetite remains concentrated in innovation-linked equities rather than cyclical consumption sectors.

A key parallel development was the sharp shift in positioning around Contemporary Amperex Technology Co., the world’s largest electric vehicle battery producer, which is dual-listed in Shenzhen and Hong Kong.

Following a large-scale share sale that expanded available float, bearish positioning against the Hong Kong-listed shares fell significantly.

Market data showed short interest dropping to its lowest level in months, as traders unwound positions that had previously profited from valuation gaps between Hong Kong and mainland listings.

The share sale itself acted as a liquidity reset.

By increasing the supply of borrowable shares, it reduced the cost of shorting and enabled hedge funds and macro traders to exit crowded bearish trades.

At the same time, it signaled continued corporate confidence in funding expansion and international growth, particularly in battery manufacturing capacity and next-generation energy storage technologies.

Importantly, the reduction in bearish bets does not imply a uniform bullish consensus.

Instead, it reflects a repositioning after a period of extreme concentration in short trades tied to valuation spreads between dual-listed Chinese equities.

With that arbitrage pressure easing, CATL’s Hong Kong shares have stabilised near elevated levels, supported by continued investor focus on electric vehicle demand, energy transition policies, and global supply chain expansion.

Across the broader market, the interaction between macro data and stock-specific flows remains decisive.

Industrial profit improvements provide a baseline signal of stabilisation, but equity performance is still heavily influenced by liquidity conditions, regulatory expectations, and global risk sentiment toward Chinese assets.

The combined effect of stronger industrial earnings signals and easing bearish pressure in key growth stocks has therefore produced a cautious but visible uplift in Hong Kong and mainland equities, with technology and advanced manufacturing sectors leading relative performance.

Market participants are now positioning around whether this phase represents a durable earnings recovery or a temporary repricing driven by liquidity shifts and short-covering activity in high-profile growth stocks.