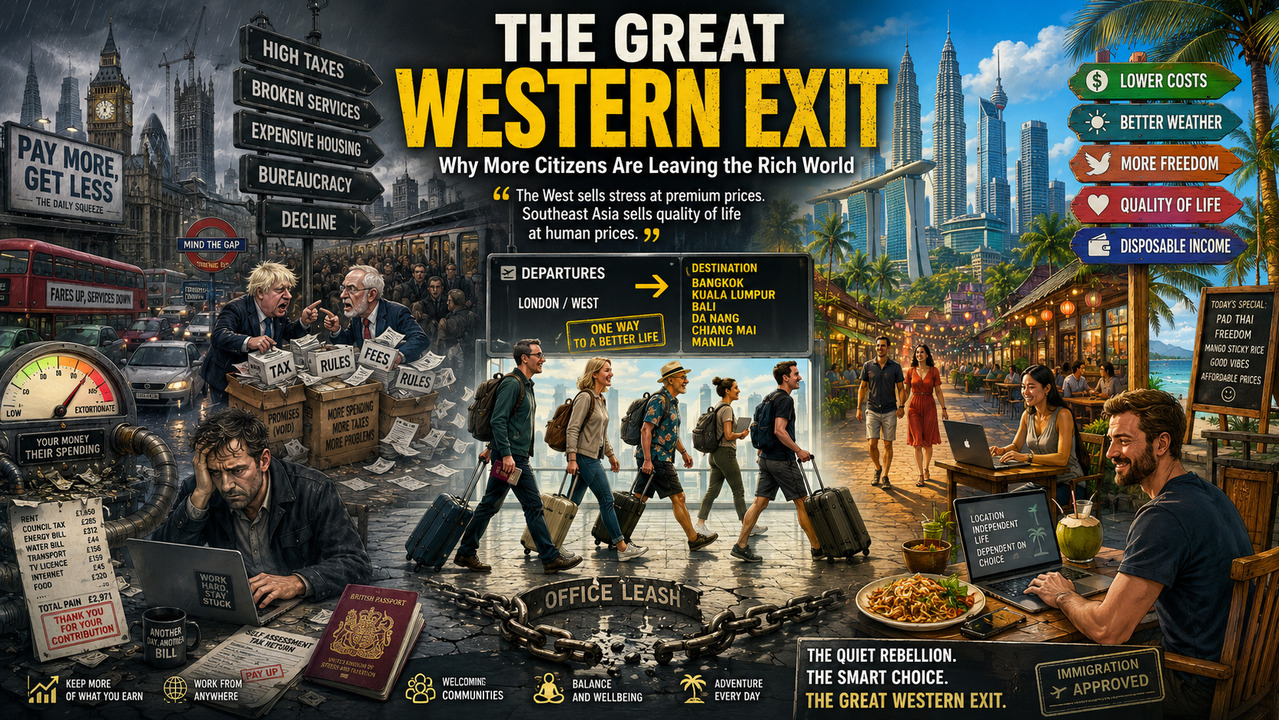

How Western governments punished competence, imported chaos, dependency, and troublemakers, drove their best citizens toward safer, freer, more comfortable, and more functional countries — and then called the collapse “progress.”

The West spent decades marketing itself as civilization’s final upgrade.

America sold the dream.

Britain sold prestige.

Canada sold politeness.

Australia sold balance.

Europe sold sophistication.

People moved there for safety, order, opportunity, clean streets, stable institutions, functioning services, and the promise that hard work still meant something.

That story is collapsing in real time.

Now the rich world is not only importing migrants.

It is bleeding its own citizens.

And the people leaving are not the failures.

They are the productive.

The skilled.

The mobile.

The ambitious.

The exhausted middle class.

The professionals who finally looked at their tax bill, rent bill, energy bill, transport bill, food bill, and political leadership and realized something brutal:

The system is consuming them faster than it rewards them.

This is not tourism.

This is not wanderlust.

This is not “finding yourself.”

This is a silent middle finger to governments that turned citizenship into a financial extraction program.

Millions are leaving wealthy countries because the deal has collapsed.

The social contract is dead.

And governments killed it themselves.

The West Became Addicted to Punishing the Productive

Western governments built entire political models around one dangerous assumption:

The productive class would never leave.

So they squeezed harder.

Higher taxes.

More regulation.

More fees.

More compliance.

More reporting.

More surveillance.

More penalties.

More guilt.

More lectures.

Every budget became a hostage note written to taxpayers.

“Pay more.”

“For fairness.”

“For healthcare.”

“For climate.”

“For inclusion.”

“For infrastructure.”

“For social justice.”

“For yesterday’s mistakes.”

“For tomorrow’s promises.”

The slogans changed.

The robbery stayed the same.

Governments discovered something politically addictive: productive citizens are easier to tax than government waste is to fix.

So instead of reforming bloated bureaucracies, they milked workers.

Instead of cutting incompetence, they taxed ambition.

Instead of reducing waste, they punished productivity.

And they did it while services got worse.

That is the part that broke people psychologically.

Citizens can survive high taxes.

What they cannot survive is paying Scandinavian-level taxation for collapsing standards, dirty streets, unaffordable housing, weak policing, overcrowded infrastructure, migration chaos, and politicians who speak like therapists while governing like accountants drunk on debt.

The insult is no longer economic.

It is moral.

People feel cheated.

And they are right.

Britain Became the Perfect Warning Sign

Britain is no longer viewed internationally as the polished center of stability and competence it once pretended to be.

It became a cautionary tale.

A country where people work harder and own less.

A country where salaries rise slower than rent.

A country where young people cannot buy homes.

A country where trains cost a fortune and still fail.

A country where taxes rise while public confidence collapses.

A country where the political class behaves like a protected aristocracy managing decline while pretending to manage recovery.

The Conservatives spent years promising discipline while producing drift, scandal, tax expansion, mass migration chaos, bureaucratic paralysis, and collapsing public trust.

Then Labour arrived promising repair while carrying the exact same addiction to taxpayer money — just wrapped in softer language and moral branding.

Both sides blame each other.

Both sides protect the machine.

Both sides feed from the same ecosystem of consultants, donors, lobbyists, public-sector managers, think tanks, media insiders, and career politicians.

Both sides grow richer while ordinary citizens grow poorer.

That is why public anger feels different now.

It is no longer frustration.

It is disgust.

People look at Westminster and no longer see leadership.

They see a corporate board of professional promise-makers managing national decline while billing the public for the experience.

Modern Corruption Does Not Hide in Dark Alleys. It Sits in Parliament.

Western corruption became sophisticated.

It stopped looking criminal.

It started looking official.

It wears tailored suits.

It speaks in policy language.

It hides behind committees, reports, inquiries, advisory panels, consultations, compliance frameworks, and endless procedural theatre.

Modern corruption is not a politician stealing cash from a safe.

Modern corruption is wasting billions with no consequences.

It is failed ministers receiving promotions.

It is lobbyists writing policy.

It is donor networks feeding legislation.

It is public contracts handed to connected insiders.

It is regulators protecting systems instead of citizens.

It is politicians becoming millionaires while preaching sacrifice to workers.

It is governments printing debt while taxing productivity.

It is leaders demanding “solidarity” from citizens while protecting themselves from the consequences of their own decisions.

And ordinary people see it clearly.

That is the political mistake elites keep making.

They think the public is stupid because the public is polite.

The public sees everything.

They see the hypocrisy.

They see the double standards.

They see the corruption hidden behind sophistication.

They see politicians entering office comfortably wealthy and leaving extraordinarily wealthy.

They see entire political careers built on managing problems that never get solved because solving them would end the funding stream.

Western politics became an industry.

Decline became a business model.

Fear became taxation fuel.

And productive citizens became livestock.

The Pandemic Destroyed the Final Illusion

Then Covid happened.

And the office lie collapsed.

For decades, millions of workers were trapped in a ridiculous ritual designed less for productivity and more for managerial control.

Wake up early.

Commute through traffic.

Sit in cubicles.

Attend meaningless meetings.

Pretend to look busy.

Spend money near the office.

Repeat until retirement.

Then lockdowns arrived and exposed the truth.

A huge percentage of modern work can be done from anywhere.

Once people discovered they could work remotely, the psychological barrier shattered instantly.

The question changed forever.

Why live in London if your laptop works in Bangkok?

Why suffer freezing rent slavery in Toronto when Kuala Lumpur offers a higher standard of living at a fraction of the cost?

Why tolerate endless stress in Britain when Thailand offers sunshine, affordability, safety, comfort, and breathing room?

The office cage opened.

Millions walked out mentally before they walked out physically.

And once a citizen emotionally detaches from the system, departure becomes logistics.

Not philosophy.

Southeast Asia Humiliated the Western Narrative

Southeast Asia did not become attractive because it is perfect.

It became attractive because it exposed how absurd the Western cost-to-quality ratio became.

That is the comparison Western governments fear most.

Not military rivals.

Not political opposition.

Comparison.

Because comparison destroys propaganda instantly.

A British professional lands in Bangkok and suddenly realizes something devastating:

Life does not have to feel like financial punishment.

The same income delivers:

Better apartments.

Better weather.

Better food.

Better healthcare access.

More convenience.

More personal freedom.

More service.

More social life.

More savings.

More breathing room.

More life.

Meanwhile, back in the West:

Higher taxes.

Higher rent.

Higher stress.

Higher energy costs.

Higher transport costs.

Higher childcare costs.

Higher food costs.

Higher anxiety.

Lower trust.

Lower optimism.

Lower quality of life.

The West sells stress at luxury prices.

Southeast Asia sells dignity at human prices.

That comparison is politically radioactive because once citizens experience it, they stop believing the old mythology.

The Western establishment still talks as if Asia is the developing world.

Meanwhile millions of Westerners now quietly view parts of Southeast Asia as the upgrade.

That is humiliating for Western leadership.

And they earned the humiliation themselves.

The Productive Are Escaping the Extraction Machine

The people leaving are not random.

They are exactly the people governments cannot afford to lose.

Engineers.

Founders.

Developers.

Consultants.

Remote workers.

Investors.

Retirees with capital.

Young professionals.

Business owners.

The welfare state depends on them.

The tax system depends on them.

The property market depends on them.

The service economy depends on them.

And governments spent years treating them like enemies.

So now they leave.

And when productive citizens leave, the damage multiplies.

The state loses future tax revenue.

Future startups.

Future spending.

Future investment.

Future children.

Future jobs.

Future economic energy.

Then the remaining population gets taxed harder to compensate.

Then more people leave.

This is how rich countries begin decaying from the inside.

Not with riots.

With airport departures.

One-way tickets.

Foreign residency permits.

Offshore companies.

Remote contracts.

And laptops opening under warmer skies.

Western Leaders Already Know All of This

That is the darkest part.

They know.

They hear the complaints.

They see the departure statistics.

They understand the collapse in trust.

They know citizens feel squeezed, betrayed, overtaxed, overregulated, overcharged, and politically abandoned.

They know housing is broken.

They know public services are deteriorating.

They know young people lost faith in ownership.

They know middle-class families feel trapped.

They know productive citizens feel hunted.

They know the exodus is real.

And they keep doing the same thing.

Why?

Because the system still works for them.

Politics became a wealth ladder.

A networking club.

A consultancy pipeline.

A media career accelerator.

A donor marketplace.

A retirement investment plan disguised as public service.

The public suffers.

The machine feeds itself.

And leadership calls this democracy.

That is why citizens are leaving.

Not because they hate their countries.

Because their countries stopped respecting them.

The Great Western Exit Is Not About Beaches

This is the biggest misunderstanding.

The exodus is not about sunshine.

It is not about cheap cocktails.

It is not about palm trees.

It is about trust collapsing between citizens and the systems ruling them.

People tolerate hardship when they believe leadership is competent and honest.

People tolerate sacrifice when they believe the system is fair.

People tolerate taxes when they receive dignity in return.

That trust is gone.

Now millions look at their governments and see something colder:

A permanent extraction machine feeding on productive citizens while rewarding incompetence, bureaucracy, ideological theatre, and political insiders.

That realization changes everything.

Because once citizens stop believing the system deserves loyalty, geography becomes optional.

And the West is discovering a terrifying truth:

In a remote-work world, productive people no longer need to stay where they are punished.

They can leave.

And increasingly, they do.

Final Warning

The Great Western Exit is not a migration trend.

It is a civilizational alarm bell.

A warning that citizens no longer believe their governments serve them.

A warning that the productive class feels hunted instead of valued.

A warning that corruption wrapped in sophistication still looks like corruption.

A warning that endless taxation without visible competence destroys trust.

A warning that countries cannot indefinitely punish ambition while expecting loyalty.

The people leaving already delivered their verdict.

The West became too expensive.

Too bureaucratic.

Too arrogant.

Too disconnected from ordinary life.

Too comfortable managing decline while calling it progress.

And now millions are responding in the only language governments truly understand:

Departure.

The productive are leaving.

The taxpayers are leaving.

The entrepreneurs are leaving.

The engineers, founders, professionals, investors, skilled workers, and educated middle class are leaving.

And Western governments are replacing loyalty, competence, stability, and contribution with uncontrolled dependency, social fragmentation, imported tensions, collapsing cohesion, and demographic policies they are too cowardly to discuss honestly with their own citizens.

The result is a civilization committing slow-motion suicide while its political class calls it “progress.”

A country cannot endlessly punish the people who build, fund, obey, innovate, and sustain society while importing chaos faster than it imports integration.

It cannot tax competence into exile and subsidize dysfunction into permanence.

It cannot survive by driving out the productive class and then pretending GDP statistics still mean civilization is healthy.

And yet Western leaders continue the same policies because the collapse has not reached their pockets, their corruption deals, their salaries, their pensions, or their security details.

Not yet.

And by the time politicians finally feel the damage themselves, the country they exploited no longer exists in a form capable of financing their corruption, their luxury, their protection, and the decadent political class that fed on its decline.

When the builders leave, the system rots from the inside.

And by the time politicians finally feel the damage themselves, the country they exploited no longer exists in a form capable of financing their corruption, their luxury, their protection, and the decadent political class that fed on its decline.

When the builders leave, the system rots from the inside.

But history is brutally clear:

When the builders leave, the system rots from the inside.

And by the time politicians finally feel the damage themselves, the country they exploited no longer exists in a form capable of financing their corruption, their luxury, their protection, and the decadent political class that fed on its decline.