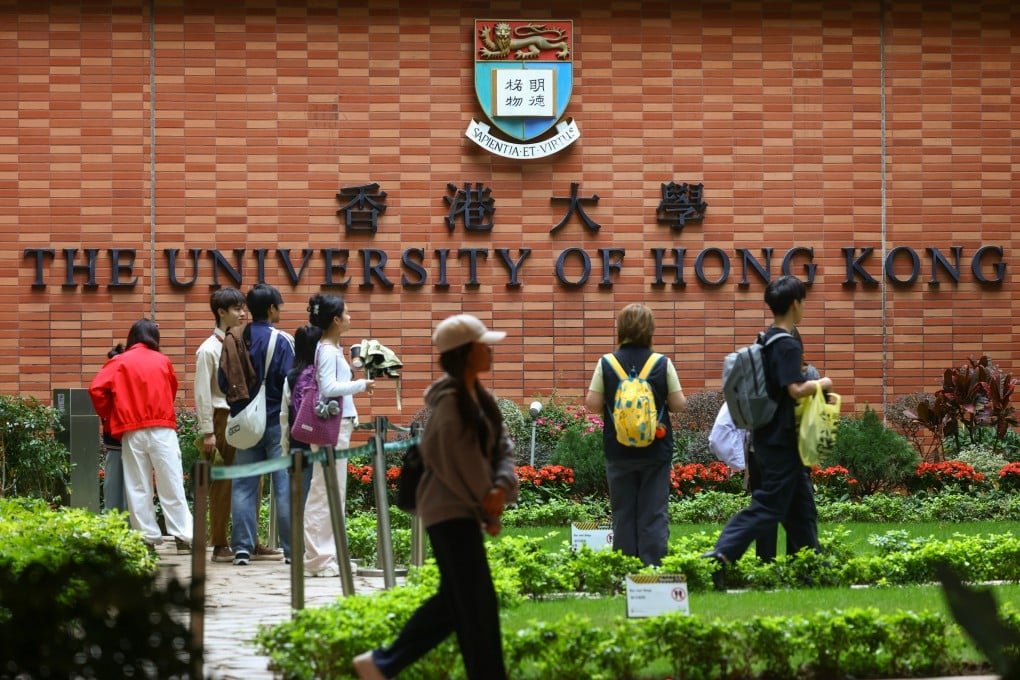

Singapore’s second-largest bank is deepening its bet on Hong Kong as competition intensifies for Asia’s wealthy clients and cross-border capital flows.

Singapore-based OCBC is accelerating its expansion in Hong Kong by planning to hire between thirty and fifty additional relationship managers in 2026, a move that reflects intensifying competition among Asian banks for wealthy clients, offshore assets, and regional investment flows.

What is confirmed is that the hiring plan represents an increase of more than thirty percent in the bank’s Hong Kong-based relationship management workforce.

The expansion is tied directly to OCBC’s wealth management strategy and its broader objective of becoming one of Hong Kong’s top ten lenders by 2030.

The story is fundamentally actor-driven because the expansion reflects a deliberate strategic decision by a major regional bank to increase market share in one of Asia’s most contested financial centers.

The hiring push is not simply about staffing levels.

It is a signal that OCBC believes Hong Kong remains central to the future of Asian private banking and cross-border wealth management despite years of political turbulence, geopolitical pressure, and competition from Singapore.

The mechanics behind the move are straightforward but significant.

Relationship managers are the core revenue engine of modern private banking.

They manage high-net-worth and affluent clients, oversee investment portfolios, distribute financial products, and help move capital across jurisdictions within regulatory limits.

Expanding this workforce indicates expectations of rising client acquisition, larger asset pools, and increased transaction activity.

OCBC’s Hong Kong operation has recently reported strong growth.

Revenue in the city rose sharply in the first quarter of 2026, while profit growth significantly outpaced revenue expansion.

Wealth management income climbed substantially, and corporate wealth business reportedly more than tripled.

These figures matter because they suggest that wealth-related businesses are now contributing disproportionately to profitability growth.

The expansion also reflects a larger regional realignment in Asian finance.

Over the past several years, Singapore and Hong Kong have competed aggressively to attract family offices, wealthy mainland Chinese clients, institutional investors, and regional corporate treasury operations.

Rather than replacing Hong Kong, Singaporean banks increasingly appear to be using both cities as complementary hubs.

Singapore provides political stability and Southeast Asian connectivity, while Hong Kong remains deeply integrated with mainland Chinese capital markets and offshore Chinese wealth.

For OCBC, Hong Kong offers access to mainland Chinese clients seeking international diversification, as well as regional investors looking for exposure to China-related assets.

The city’s role as a gateway to China continues to generate strategic value for banks even as broader geopolitical tensions reshape global finance.

The hiring plan also highlights the continued resilience of Hong Kong’s financial sector.

International headlines over recent years often focused on political tightening and slowing property markets.

Yet major banks continue to invest heavily in wealth management operations there because client assets, trading flows, and demand for sophisticated financial services remain substantial.

Competition, however, is becoming more intense.

Regional and global banks are all expanding private banking capabilities across Asia, creating a battle for experienced relationship managers who can bring established client books with them.

Compensation costs have risen, and talent mobility across Singapore, Hong Kong, and mainland China has become increasingly important to growth strategies.

Another layer to the story is demographic and geographic wealth expansion.

Asian private wealth continues to grow faster than many Western markets, driven by entrepreneurs, technology founders, manufacturing executives, and multigenerational family businesses.

Banks are racing to secure long-term relationships before wealth transfers reshape client loyalties over the next decade.

OCBC’s strategy also includes physical modernization.

The bank has indicated plans to upgrade branch infrastructure and expand premium client facilities in Hong Kong.

This reflects a broader industry shift in which banks increasingly combine digital platforms with high-touch advisory services aimed at affluent customers.

The broader implication is that Asian banking competition is entering a more aggressive phase centered on wealth management rather than traditional lending alone.

Banks now view affluent clients not simply as deposit holders but as long-term ecosystems generating investment fees, insurance sales, lending opportunities, and cross-border transaction business.

In practical terms, OCBC’s hiring expansion reinforces confidence in Hong Kong’s continued role as a regional financial hub while underscoring how aggressively Asian banks are positioning for the next cycle of wealth accumulation and capital mobility across the region.

What is confirmed is that the hiring plan represents an increase of more than thirty percent in the bank’s Hong Kong-based relationship management workforce.

The expansion is tied directly to OCBC’s wealth management strategy and its broader objective of becoming one of Hong Kong’s top ten lenders by 2030.

The story is fundamentally actor-driven because the expansion reflects a deliberate strategic decision by a major regional bank to increase market share in one of Asia’s most contested financial centers.

The hiring push is not simply about staffing levels.

It is a signal that OCBC believes Hong Kong remains central to the future of Asian private banking and cross-border wealth management despite years of political turbulence, geopolitical pressure, and competition from Singapore.

The mechanics behind the move are straightforward but significant.

Relationship managers are the core revenue engine of modern private banking.

They manage high-net-worth and affluent clients, oversee investment portfolios, distribute financial products, and help move capital across jurisdictions within regulatory limits.

Expanding this workforce indicates expectations of rising client acquisition, larger asset pools, and increased transaction activity.

OCBC’s Hong Kong operation has recently reported strong growth.

Revenue in the city rose sharply in the first quarter of 2026, while profit growth significantly outpaced revenue expansion.

Wealth management income climbed substantially, and corporate wealth business reportedly more than tripled.

These figures matter because they suggest that wealth-related businesses are now contributing disproportionately to profitability growth.

The expansion also reflects a larger regional realignment in Asian finance.

Over the past several years, Singapore and Hong Kong have competed aggressively to attract family offices, wealthy mainland Chinese clients, institutional investors, and regional corporate treasury operations.

Rather than replacing Hong Kong, Singaporean banks increasingly appear to be using both cities as complementary hubs.

Singapore provides political stability and Southeast Asian connectivity, while Hong Kong remains deeply integrated with mainland Chinese capital markets and offshore Chinese wealth.

For OCBC, Hong Kong offers access to mainland Chinese clients seeking international diversification, as well as regional investors looking for exposure to China-related assets.

The city’s role as a gateway to China continues to generate strategic value for banks even as broader geopolitical tensions reshape global finance.

The hiring plan also highlights the continued resilience of Hong Kong’s financial sector.

International headlines over recent years often focused on political tightening and slowing property markets.

Yet major banks continue to invest heavily in wealth management operations there because client assets, trading flows, and demand for sophisticated financial services remain substantial.

Competition, however, is becoming more intense.

Regional and global banks are all expanding private banking capabilities across Asia, creating a battle for experienced relationship managers who can bring established client books with them.

Compensation costs have risen, and talent mobility across Singapore, Hong Kong, and mainland China has become increasingly important to growth strategies.

Another layer to the story is demographic and geographic wealth expansion.

Asian private wealth continues to grow faster than many Western markets, driven by entrepreneurs, technology founders, manufacturing executives, and multigenerational family businesses.

Banks are racing to secure long-term relationships before wealth transfers reshape client loyalties over the next decade.

OCBC’s strategy also includes physical modernization.

The bank has indicated plans to upgrade branch infrastructure and expand premium client facilities in Hong Kong.

This reflects a broader industry shift in which banks increasingly combine digital platforms with high-touch advisory services aimed at affluent customers.

The broader implication is that Asian banking competition is entering a more aggressive phase centered on wealth management rather than traditional lending alone.

Banks now view affluent clients not simply as deposit holders but as long-term ecosystems generating investment fees, insurance sales, lending opportunities, and cross-border transaction business.

In practical terms, OCBC’s hiring expansion reinforces confidence in Hong Kong’s continued role as a regional financial hub while underscoring how aggressively Asian banks are positioning for the next cycle of wealth accumulation and capital mobility across the region.